Two GST Changes Went Live 36 Days Ago. One Freezes Your Return. The Other Is Rs 10,000 Per Invoice. Have You Acted on Either?

Published on:

Category: Compliance & Taxation

Author: WeConsult India Desk

The Story :

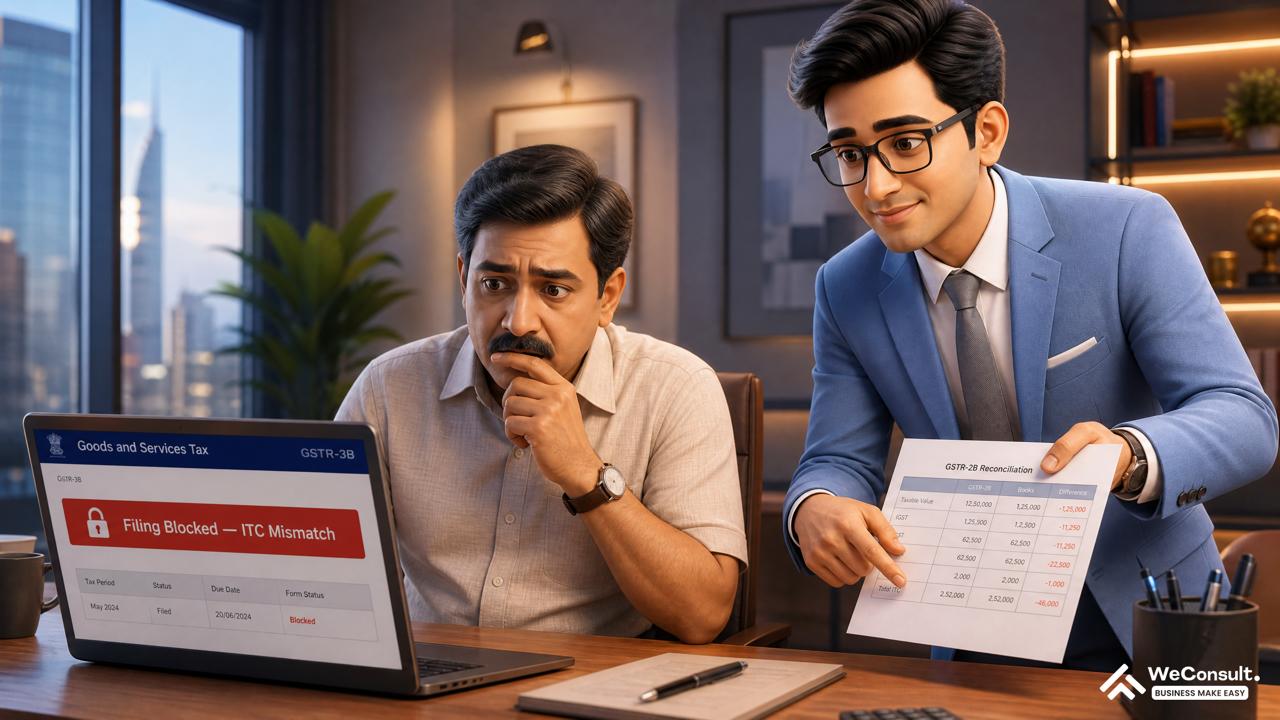

Deepak runs a mid-sized trading business in Gurugram's Udyog Vihar. He has been filing GST returns since 2017 — never missed a GSTR-3B, always deposited on time. His turnover crossed Rs 6 crore in FY 2025-26.

On May 20, 2026 — when his April GSTR-3B is due — he will log into the GST portal and attempt to file. If his ITC claims in GSTR-3B do not exactly match the figures auto-populated in his GSTR-2B, the portal will block his filing entirely.

Not flag it. Not warn him. Block it.

There is a second problem. Since April 1, 2026, every B2B invoice Deepak has raised must carry an Invoice Reference Number (IRN) generated from the IRP. Without an IRN, the invoice is non-compliant under Section 122 of the CGST Act. The penalty: Rs 10,000 per invoice or 100% of the tax amount — whichever is higher.

Deepak has been raising invoices the same way he always has. His billing software was not updated. Thirty-six days of invoices. Each one potentially non-compliant.

The Real Problem — Why Most Business Owners Haven't Acted Yet

Both changes were announced well in advance. But between notification issued and business owner updates their process is a gap that the GST system has always struggled to close.

The ITC hard block is particularly dangerous because it looks like a technical glitch the first time it triggers. Most business owners — and many accountants — will assume the portal is having an issue and wait for it to resolve. It is not a glitch. It is the new normal.

Under the old system, the GST portal was like a bank that processed your deposit even if there was a discrepancy in your paperwork — flagging it for review later. Under the new system, the bank rejects the deposit at the counter until the paperwork is exactly right. Every day the deposit sits unprocessed, interest accrues at 18% per annum.

The Law Explained Simply — Two Changes, Both Live from April 1, 2026

Change 1: ITC Hard Block — GSTR-2B vs GSTR-3B mismatch now freezes your return.

If your claimed ITC in GSTR-3B exceeds your GSTR-2B auto-populated ITC by even a single rupee — the portal blocks the filing. The three most common triggers: (1) Supplier filed GSTR-1 late or not at all — their invoice doesn't appear in your GSTR-2B. (2) Invoice timing difference — supplier uploaded the invoice in the next month's GSTR-1. (3) Wrong GSTIN on the invoice — credit doesn't map to your account.

The Invoice Management System (IMS) is the companion tool. Any invoice your supplier uploads to GSTR-1 appears in your IMS dashboard. If you take no action, it is treated as deemed accepted and flows into GSTR-2B. Unreviewed invoices that auto-flow cannot be reversed after the filing cycle closes.

Change 2: E-Invoicing mandatory for AATO above Rs 5 crore from April 1, 2026 — reduced from the earlier Rs 10 crore threshold.

Every B2B invoice, credit note, and debit note issued from April 1, 2026 must carry a valid IRN generated from the IRP. E-invoicing does not change your invoice format — it adds an IRN generation step before the invoice is issued to the buyer.

|

Non-Compliance Situation |

Legal Consequence |

|

B2B invoice without IRN after April 1, 2026 |

Not a valid tax invoice — buyer cannot claim ITC on it |

|

Penalty on seller under Section 122 CGST Act |

Rs 10,000 per invoice OR 100% of the tax amount — whichever is HIGHER |

|

Rs 10 lakh invoice with 18% GST |

Tax = Rs 1.8 lakh. Penalty = Rs 1.8 lakh (100% of tax — exceeds Rs 10,000 flat) |

|

Rs 50,000 invoice with 18% GST |

Tax = Rs 9,000. Penalty = Rs 10,000 (flat minimum — exceeds 100% of tax) |

|

ITC Hard Block — GSTR-3B vs GSTR-2B mismatch |

Filing blocked — cannot pay GST liability legitimately until mismatch cleared. Interest at 18% per annum on outstanding tax |

|

IMS unreviewed invoice — no action taken |

Deemed accepted at end of filing cycle — cannot be reversed or rejected after IMS window closes |

Deepak vs Meena — The Same Turnover, Two Very Different May 20 Experiences

Meena's GST consultant updated her IRP integration in March 2026. From April 1, every invoice raised in Tally was automatically routed through the IRP before printing. IRN generated, QR code embedded. Her IMS dashboard: reviewed weekly since April 1. Her GSTR-2B: clean, reconciled, matching her GSTR-3B claim before May 15. May 20: filed GSTR-3B in 12 minutes. No blocks. No interest.

Deepak's software was not updated. His April invoices: no IRN, no QR code — 36 days of non-compliant invoices to 14 buyers. His IMS dashboard had 23 pending invoices — auto-accepted, several duplicates. His GSTR-3B ITC claim was Rs 1.4 lakh higher than GSTR-2B because one major supplier had not filed their April GSTR-1. May 20: filing blocked. Three days of chasing suppliers and clearing mismatches. Filed May 23. Late by 3 days. Interest: ~Rs 8,000.

The difference between Deepak and Meena is not their turnover or their tax liability. It is a software configuration that took Meena's consultant four hours to complete in March.

How to Actually Start — 5 Steps to GST Compliance Under the New Regime

1. Step 1 — Check whether your AATO crossed Rs 5 crore in FY 2025-26 — Log into the GST portal, your GSTIN, Annual Aggregate Turnover. If FY 2025-26 AATO is Rs 5 crore or above — e-invoicing is mandatory from April 1, 2026. If below Rs 5 crore, not yet mandatory — but check monthly as you approach the threshold.

2. Step 2 — Configure your accounting software for IRP integration today — If you use Tally Prime, Zoho Books, Busy Accounting, MARG ERP, or any major Indian accounting software — the IRP integration module is already available. Activate the e-invoicing module, enter your GSTIN and API credentials from the GST portal under e-invoice API access, and test-generate one IRN on a sandbox invoice. If your software does not support IRP integration natively, use the government's free IRP portal at einvoice1.gst.gov.in.

3. Step 3 — Review your IMS dashboard at least weekly before the GSTR-3B filing date — Log into the GST portal — Invoice Management System. For every invoice from your suppliers: accept valid ones, reject incorrect ones. The critical rule: if you take no action, the invoice is deemed accepted at end of the filing cycle. You cannot undo a deemed acceptance after the IMS window closes for that period.

4. Step 4 — Reconcile GSTR-2B with your purchase register before filing GSTR-3B — Pull your GSTR-2B for April 2026. Compare it line-by-line with your purchase register and GSTR-3B ITC claim. If any supplier's invoice appears in your register but not in GSTR-2B — the supplier has not filed their GSTR-1 yet. Under the ITC hard block, two options: (a) defer that ITC to May and file GSTR-3B without it, or (b) contact the supplier and ask them to file GSTR-1 before May 20. Option (a) is safer for your filing deadline.

5. Step 5 — If you have raised B2B invoices without IRNs since April 1 — regularise them now — Consult your GST consultant on whether back-dating IRN generation is possible for affected invoices. Do not wait for an enforcement notice. Voluntary correction before a notice significantly reduces penalty exposure and demonstrates compliance intent.

Your GSTR-3B is not just a return. It is a compliance statement that, from April 2026, the portal can validate in real time against your supplier data.

Key Takeaways

|

Key Compliance Point |

What You Must Do |

|

ITC Hard Block is live — GSTR-3B filing blocked if ITC > GSTR-2B |

Reconcile GSTR-2B with purchase register before May 20. Defer any unmatched ITC — do not claim what is not in GSTR-2B |

|

IMS dashboard unreviewed invoices = deemed accepted |

Review IMS weekly — accept valid invoices, reject incorrect ones before the cycle closes each month |

|

E-invoicing mandatory for Rs 5 crore+ AATO from April 1, 2026 |

Configure IRP integration in accounting software immediately. All April invoices without IRN are exposed to Rs 10,000/invoice penalty |

|

Supplier non-filing = your ITC blocked, not theirs |

Track high-value supplier GSTR-1 filing status before your own filing date every month |

But Here Is the Other Side…

But here is the other side: the ITC hard block and the IMS system, taken together, are a genuine simplification for businesses that maintain disciplined purchase registers. In the old system, ITC mismatches could accumulate for months before a reconciliation statement or scrutiny notice revealed them — often creating large, unexpected tax demands. The new system surfaces mismatches in real time, every month. A business that reviews its IMS weekly and reconciles GSTR-2B before filing will almost never face a disputed ITC claim. The ITC hard block is painful in the first few months of transition. It is structurally cleaner than what it replaced.

One Last Thing — The Portal Is Not Having a Glitch. This Is the New System.

When Deepak's GSTR-3B filing is blocked on May 20, his first instinct will be to call his accountant and ask if the portal is down. It is not. This is the new filing experience.

The IMS dashboard review, the GSTR-2B reconciliation before filing, and the IRP integration for e-invoicing — these are not temporary adjustments. They are the permanent operating reality for every GST-registered business above the relevant thresholds from April 1, 2026.

The businesses that update their processes in May will file June smoothly. The ones that don't will repeat this exercise — with compounding interest — every month until they do.

WeConsult India manages monthly GST compliance — GSTR-1, GSTR-3B, IMS dashboard review, GSTR-2B reconciliation, and e-invoicing setup — for businesses across Gurugram's Udyog Vihar, Sector 37, and IMT Manesar. If your April 2026 GSTR-3B is at risk of blocking — contact us before May 20.

Stay compliant. Stay protected. — WeConsult India

This blog is for informational purposes only and does not constitute legal or professional advice. Please consult a qualified Company Secretary or Chartered Accountant before acting on any compliance matter.

Related Blogs

More articles from the compliance & taxation.

Compliance & Taxation

India's Buyback Tax Changed Three Times in 18 Months. Here Is Which Rule Applies to Your Situation Right Now.

The Story: Vikram is a director and minority shareholder of a private limited company in Gurugram. In November 2024, the company offered to buy back shares from existing shareholders. A colleague who had participated in a different company's buyback in August 2024 had paid zero tax on the proceeds. Vikram, participating in November 2024, received his buyback proceeds and discovered that the full amount was taxable as deemed dividend income at his slab rate. He paid Rs 8.4 lakh in tax on Rs 20 lakh of proceeds. His Rs 6 lakh cost of acquisition became a capital loss — usable only against other capital gains, of which he had none. Same type of transaction. Same company structure. Different month. Different rule. Now it is May 2026. Vikram's company is planning another buyback. The Finance Act 2026 changed the rules again from April 1, 2026. This blog maps all three regimes and answers which one applies to your situation right now. The Real Problem — Why Three Different Rules in 18 Months The confusion around buyback taxation is the result of three successive policy reversals, each responding to a problem created by the previous one. Think of it like a road that was first toll-free, then had a toll imposed on drivers, then was changed to toll on the cargo, and is now back to a toll on drivers — but only on the premium cargo. The governing rule for your buyback is determined not by the company's incorporation date, not by your shareholding percentage, and not by when you originally bought the shares. It is determined by the date the company makes the buyback payment to you. That date — and only that date — determines which of the three regimes applies. The Law Explained Simply — Three Regimes, Three Outcomes Regime When It Applies Who Pays Tax On What Amount Regime 1 Buybacks paid on or before Sept 30, 2024 Company pays 23.3% buyback tax (Section 115QA) Full distributed amount — shareholder receives tax-free. Cost = capital loss in shareholder's hands. Regime 2 Buybacks paid Oct 1, 2024 to March 31, 2026 Shareholder at income tax slab rate (up to 42.74%) FULL buyback proceeds taxed as deemed dividend. Cost separately = capital loss (no immediate offset for most). Regime 3 Buybacks paid from April 1, 2026 onwards Shareholder at capital gains rates. Promoters: effective 30% (individuals) / 22% (companies). GAIN ONLY (proceeds minus cost of acquisition). LTCG 12.5% (12+ months). STCG 20%. Regime 1 Detail: Pre-October 2024 Under Section 115QA of the Income Tax Act, 1961, companies paid a flat tax of 20% plus 12% surcharge and 4% cess (effective approximately 23.3%) on the amount distributed in a buyback. Shareholders received proceeds tax-free. The cost of acquisition was treated as a capital loss in shareholders' hands, usable against other capital gains. Regime 2 Detail: October 2024 — March 2026 (The Deemed Dividend Problem) The Finance Act, 2024, abolished Section 115QA from October 1, 2024. Under this regime: company paid zero tax; full buyback proceeds treated as deemed dividend in the shareholder's hands; taxed at slab rate (up to 30% plus surcharge and cess = up to 42.74%). Cost of acquisition became a separate capital loss. The problem: a shareholder who paid Rs 100 per share and received Rs 300 in a buyback faced tax on the full Rs 300 as dividend income. The Rs 100 cost became a capital loss usable only against other capital gains, which many small investors did not have. Regime 3 Detail: From April 1, 2026 (Finance Act 2026) Finance Act 2026, via Section 69 of the Income Tax Act, 2025, restores capital gains treatment. Tax only on the actual gain (buyback price received minus cost of acquisition). LTCG at 12.5% for shares held 12+ months. STCG at 20%. No company-level tax. Promoter additional levy: To prevent promoters from using buybacks as a lower-tax exit route, Finance Act 2026 imposes a Special Additional Tax on promoters. Effective rate: 30% for individual / non-corporate promoters; 22% for domestic corporate promoters. For unlisted private limited companies, promoter includes anyone with 10%+ direct or indirect shareholding or classified as promoter under Section 2(69) of the Companies Act, 2013. Promoter Type Normal CG Tax Additional Levy Effective Rate Individual / non-corporate promoter 12.5% LTCG / 20% STCG Additional levy to total 30% 30% effective on capital gains Domestic corporate promoter At applicable corporate CG rates Additional levy to total 22% 22% effective on capital gains Non-promoter shareholder (below 10% holding) 12.5% LTCG / 20% STCG No additional levy 12.5% or 20% on actual gain only Vikram vs Ananya — Same Economics, Very Different Tax Bills Both Vikram and Ananya hold shares in private limited companies. Both receive Rs 20 lakh in buyback proceeds. Both acquired shares at Rs 6 lakh. Both held shares for more than 24 months. Capital gain: Rs 14 lakh in both cases. Vikram's November 2024 buyback (Regime 2): Taxable as deemed dividend on Rs 20 lakh (full proceeds) at 30% slab + cess = approximately Rs 8.4 lakh tax. Capital loss of Rs 6 lakh carried forward, unusable immediately. Net received after tax: Rs 11.6 lakh. Ananya's May 2026 buyback (Regime 3, non-promoter): Taxable as LTCG on Rs 14 lakh (gain only). Less Rs 1.25 lakh annual exemption = Rs 12.75 lakh taxable. At 12.5% LTCG = approximately Rs 1.59 lakh tax. Cost fully offset within the computation. Net received after tax: Rs 18.41 lakh. Same transaction. Same underlying economics. Rs 6.8 lakh difference in tax paid. The difference is which date the payment was received. How to Actually Start — 5 Things Every Director and Shareholder Must Do Before a 2026 Buyback: 1. Step 1 — Confirm the buyback payment date, not the board resolution date — The tax regime is determined by the date the company actually makes payment to the shareholder — not the date the buyback board resolution was passed, not the date the offer opened, and not the date you tendered shares. If your company passed a buyback resolution in January 2026 but will make payment in May 2026, Regime 3 applies. Confirm the payment date with your company secretary before calculating tax liability. 2. Step 2 — Determine whether you qualify as a promoter in your specific company structure — For unlisted private limited companies, the 30% effective promoter rate applies to anyone holding more than 10% shareholding directly or indirectly, or classified as a promoter under Section 2(69) of the Companies Act. Calculate your direct and indirect shareholding before assuming you are a regular shareholder. If you hold 8% directly but your spouse holds 5% and you share economic interest, your combined indirect holding may exceed 10%. 3. Step 3 — Verify your holding period for LTCG vs STCG classification — For LTCG treatment at 12.5%, shares must have been held for more than 12 months at the time of buyback payment. Calculate the exact holding period from the date of original acquisition to the date of buyback payment. If you are close to the 12-month mark, waiting a few additional weeks before the company completes payment may shift you from STCG (20%) to LTCG (12.5%). 4. Step 4 — Verify your TDS position under the new regime — Under Regime 2, companies deducted TDS on buyback proceeds as deemed dividend TDS. Under Regime 3, buyback proceeds are capital gains — generally not subject to TDS for resident shareholders in listed company transactions. For unlisted company buybacks and NRI shareholders, TDS treatment may be different. If there is a TDS mismatch between how the company processed the payment and how it should be reported in your ITR, reconcile with your CA before filing. 5. Step 5 — Plan your ITR for Tax Year 2026-27 to include buyback capital gains correctly — Under Regime 3, your buyback gain will appear in your ITR under the capital gains schedule — not the dividend income schedule. If your company's TDS was deducted as dividend TDS (Regime 2 procedures) for a payment that falls under Regime 3, there will be a mismatch in your Form 26AS. Work with your CA to ensure the correct schedule is used and TDS credit claims match the nature of income reported. For promoters, the additional buyback tax must be correctly computed and reported separately. Your buyback proceeds are not just a financial event — they are a compliance event that requires the correct regime identification before a single number is calculated. Key Takeaways Key Compliance Point What You Must Do Regime 3 applies from April 1, 2026 — buyback proceeds are capital gains, not deemed dividend Confirm buyback payment date before calculating tax. Regime is determined by payment date only Non-promoter shareholders pay 12.5% LTCG or 20% STCG on the gain only Calculate holding period from acquisition to payment date — 12+ months = LTCG; below 12 months = STCG Promoters in unlisted companies include anyone with 10%+ direct or indirect shareholding Calculate your effective shareholding including indirect holdings before assuming non-promoter status Regime 2 buybacks (Oct 2024-Mar 2026) were taxed on full proceeds as dividend — check TDS certificates match ITR Confirm ITR schedule and TDS credit matching with your CA for any buybacks received between October 2024 and March 2026 But Here Is the Other Side… But here is the other side: Regime 3 is not better than all prior regimes for every shareholder. Under Regime 1 (pre-October 2024), shareholders received proceeds completely tax-free because the company paid the buyback tax at 23.3%. Under Regime 3, shareholders pay 12.5% LTCG or 20% STCG on the gain. For shareholders who bought shares near the buyback price (small gain relative to proceeds), Regime 3 is significantly better than Regime 2. For shareholders who received large buyback premiums in the pre-October 2024 period and paid no tax at all, Regime 3 represents a higher effective burden. Regime 3 is the most equitable framework for retail investors — but equitable is not the same as cheapest. One Last Thing — The Date on the Cheque Is the Rule That Applies: India's buyback tax history is a reminder that tax planning around a corporate event cannot be done in isolation from the regulatory environment at the time of execution. The board resolution that authorised Vikram's November 2024 buyback was drafted in September 2024 — when the rules suggested shareholders might pay no tax. By the time payment was made, the rules had changed. The Finance Act 2026 restores logical capital gains treatment to buybacks. For promoters and directors with significant shareholdings in their own companies, the additional levy is a real cost that must be factored into any buyback decision from April 2026 onwards. WeConsult India advises companies across Gurugram's Sector 82, Sector 84, and the Cyber Hub corridor on buyback structuring, tax computation, and Companies Act compliance for buyback offers. If your company is planning a buyback in Tax Year 2026-27, contact us before the board resolution is drafted. Stay compliant. Stay protected. — WeConsult India This blog is for informational purposes only and does not constitute legal or professional advice. Please consult a qualified Company Secretary or Chartered Accountant before acting on any compliance matter.

Compliance & Taxation

MCA21 V3 Portal Enhancements — Navigating the New Era of Annual Filing

Compliance Bulletin 2026 1. The Compliance Crisis: Why CCFS-2026 Matters Now Expert Analysis by The WeConsult India Desk For many Indian business owners, the "ROC filing" is that one task that keeps getting pushed to the next quarter. But as the quarters turn into years, the additional fees don't just add up—they multiply. By 2026, thousands of active and dormant companies found themselves in a compliance deadlock, unable to file current documents because of the massive backlog of penalties from previous years. The Ministry of Corporate Affairs (MCA) has recognized this bottleneck. On February 25, 2026, the MCA issued General Circular No. 01/2026, announcing the Companies Compliance Facilitation Scheme (CCFS) 2026 . This isn't just another extension; it is a strategic "clean slate" initiative designed to bring every Indian company back into the fold of active compliance. 2. What Exactly is CCFS-2026? The CCFS-2026 is a one-time amnesty scheme that allows defaulting companies to file their overdue documents by paying only a fraction of the usual additional fees. Specifically, the scheme offers a 90% waiver on the additional fees that would otherwise be payable under Section 403 of the Companies Act, 2013. Starting from April 15, 2026, and running until July 15, 2026 , companies have a 90-day window to regularize their status. This scheme covers almost all annual filings, including financial statements (AOC-4) and annual returns (MGT-7). 3. The "90% Waiver" Math: A Real-World Example Imagine a company, "Alpha Tech Pvt Ltd," with 3 years of delays across two primary forms (AOC-4 and MGT-7). Under normal circumstances, penalties could exceed ₹2,00,000 . Standard Penalty ₹2,00,000 → CCFS-2026 Fee ₹20,000 4. Who Can Benefit? (Eligibility Criteria) It applies to any "defaulting company"—active or dormant. However, exclusions apply for companies already ordered for strike-off, involved in fraud litigation, or those that have already applied for voluntary strike-off. 5. The Immunity Clause: Protection from Prosecution One of the most powerful features is the Immunity from Prosecution. Once overdue documents are filed and fees paid, the MCA will grant immunity from any prosecution or proceedings for the imposition of penalties related to those specific delays. 6. The Step-by-Step Filing Process Identify all pending forms and calculate normal fees. File forms through MCA21 V3 portal during the window (April 15 – July 15). File a separate application for the Immunity Certificate . 7. Why You Shouldn't Wait Until July Waiting until the final weeks is high-risk due to portal traffic surges, payment failures, and professional certification backlogs. Starting your audit now ensures you are first in line. 8. The Cost of Ignoring This Opportunity Once CCFS-2026 concludes on July 15, the 90% waiver disappears. More importantly, the MCA has signaled a massive "Clean Up" drive post-scheme, involving mass disqualification of directors and striking off of companies. 9. Impact on Dormant and Inactive Companies For inactive companies wishing to restart or even those intending to close legally, CCFS-2026 is the perfect bridge to clear records cost-effectively without leaving legal liabilities. 10. The Role of Digital Compliance in 2026 The MCA21 V3 portal now uses data analytics to automatically flag inconsistencies. This scheme is effectively the "last call" for manual regularization before compliance becomes even more rigid. 11. Smart Money Moves for Directors Audit Your Dashboard: List every pending form and penalty. Allocate the 10%: Set aside funds for payments by April 15. Update Your KYC: Ensure DINs are active via DIR-3 KYC. 12. Frequently Asked Questions (FAQs) Q: Does CCFS-2026 apply to LLPs? A: A parallel scheme for LLPs is often announced; check for updates. Q: Can I file for FY 2025-26? A: No, the scheme is for overdue filings from previous years. Q: What if my company is already in litigation? A: You can still file, but pending appeals may need to be withdrawn. 13. The Big Picture: India's Corporate Governance Shift CCFS-2026 reflects a "facilitation" model, helping companies focus on growth. However, once this "clean slate" is provided, future tolerance for non-compliance will be zero. 14. Bottom Line The MCA CCFS-2026 is a rare second chance in corporate law. With a 90% waiver and full immunity, there is no logical reason to remain non-compliant. Stay compliant. Stay ahead. — The WeConsult India Desk

Compliance & Taxation

Proprietorship Compliance in India (2026): Complete Legal & Tax Guide for Business Owners

Starting a sole proprietorship in India is procedurally simple — but maintaining proper proprietorship compliance is essential for legal protection, financial credibility, and sustainable business growth. Since a sole proprietorship does not have a separate legal identity, the owner bears unlimited liability. All tax and regulatory obligations directly impact the proprietor’s personal financial standing. In 2026, AI-driven tax analytics, GST auto-reconciliation, and inter-departmental data integration have made compliance more structured and strictly monitored. This detailed guide by WeConsultIndia outlines every mandatory compliance requirement applicable to proprietorship firms in India. 1. Income Tax Compliance for Proprietorship Firms Income Tax Return (ITR) filing is the foundation of sole proprietorship compliance. 📄 Applicable ITR Forms: 🔹 ITR-3 – For proprietors maintaining books and subject to audit 🔹 ITR-4 – For presumptive taxation under Sections 44AD / 44ADA ✅ Key Income Tax Compliance Requirements: ✔ Timely filing of Income Tax Return ✔ Payment of advance tax (if applicable) ✔ Compliance with tax audit provisions ✔ Accurate disclosure of all income sources ⚠ Consequences of Non-Compliance: ❌ Late filing fees under Section 234F ❌ Interest under Sections 234A, 234B, 234C ❌ Scrutiny assessment notices ❌ Financial penalties Proper income tax compliance improves creditworthiness and strengthens business credibility. 2. GST Compliance for Proprietorship Businesses GST registration becomes mandatory once turnover crosses statutory thresholds (₹20 lakh / ₹40 lakh depending on business type and state). 📌 GST Registration Also Required For: 🔹 Interstate supply of goods or services 🔹 E-commerce sellers 🔹 Claiming Input Tax Credit (ITC) 📊 Mandatory GST Filings: ✔ GSTR-1 – Outward supply details ✔ GSTR-3B – Monthly summary return ✔ Annual return (if applicable) 🚨 Risks of GST Non-Compliance: ❌ Late fees and interest ❌ Blocking of e-way bills ❌ GST registration cancellation ❌ Departmental investigation With automated GST and income tax data matching in 2026, accurate reconciliation is critical. 3. TDS Compliance Requirements TDS provisions apply when a proprietorship: 🔹 Pays salary 🔹 Makes contractor payments 🔹 Pays professional or consultancy fees 🔹 Pays rent beyond prescribed limits 📌 TDS Compliance Includes: ✔ Deduction at applicable rates ✔ Timely deposit with government ✔ Quarterly TDS return filing ✔ Issuance of Form 16 / 16A Non-compliance may result in penalties, interest, and prosecution in serious cases. 4. Maintenance of Books of Accounts Bookkeeping is both a statutory obligation and a strategic necessity. 📌 Mandatory When: 🔹 Income exceeds prescribed limits 🔹 Tax audit provisions apply 📈 Benefits of Proper Bookkeeping: ✔ Accurate ITR filing ✔ Smooth GST reconciliation ✔ Reduced compliance notices ✔ Better financial planning ✔ Improved business valuation Professional accounting supervision minimizes compliance risks significantly. 5. Tax Audit Requirements A proprietorship may require tax audit if: 🔹 Turnover exceeds statutory limits 🔹 Presumptive taxation conditions are violated 🎯 Audit Ensures: ✔ Financial transparency ✔ Correct income reporting ✔ Legal protection ✔ Risk mitigation Failure to comply can attract penalties under Section 271B. 6. Additional Regulatory Compliance Depending on business activity, additional compliance may include: ✔ Udyam (MSME) Registration ✔ Shop & Establishment Registration ✔ Professional Tax Registration ✔ EPF & ESI Registration ✔ Industry-specific licenses (FSSAI, IEC, etc.) Ignoring these obligations often results in operational disruption and penalties. Why Proprietorship Compliance Is Critical in 2026 Government systems now automatically compare: 🔍 GST returns vs Income Tax returns 🔍 TDS filings vs declared income 🔍 Bank transactions vs reported turnover Benefits of Proactive Compliance: ✔ Avoid penalties and litigation ✔ Enhance business credibility ✔ Secure funding and loans easily ✔ Ensure sustainable growth ✔ Maintain regulatory peace of mind Common Compliance Mistakes by Sole Proprietors ❌ Mixing personal and business finances ❌ Delayed GST filing ❌ Ignoring advance tax payments ❌ Not reconciling GSTR-2A / 2B ❌ Missing TDS deadlines Systematic compliance management prevents costly legal exposure. How WeConsultIndia Supports Proprietorship Compliance Managing regulatory compliance while scaling business operations can be overwhelming. At WeConsultIndia ( www.weconsultindia.in ) , we provide: ✔ Income tax filing & advisory ✔ GST registration & return filing ✔ TDS compliance management ✔ Tax audit coordination ✔ Notice handling & representation ✔ Regulatory advisory support Our structured compliance framework ensures accuracy, transparency, and complete legal protection. Final Conclusion Proprietorship compliance in India is not merely a statutory formality — it is the backbone of financial stability and long-term business success. From income tax and GST compliance to TDS obligations and audit requirements, every element contributes to risk-free operations. In the digitally monitored regulatory ecosystem of 2026, compliance must be proactive, strategic, and professionally managed. For expert compliance support, connect with WeConsultIndia and safeguard your business with confidence.