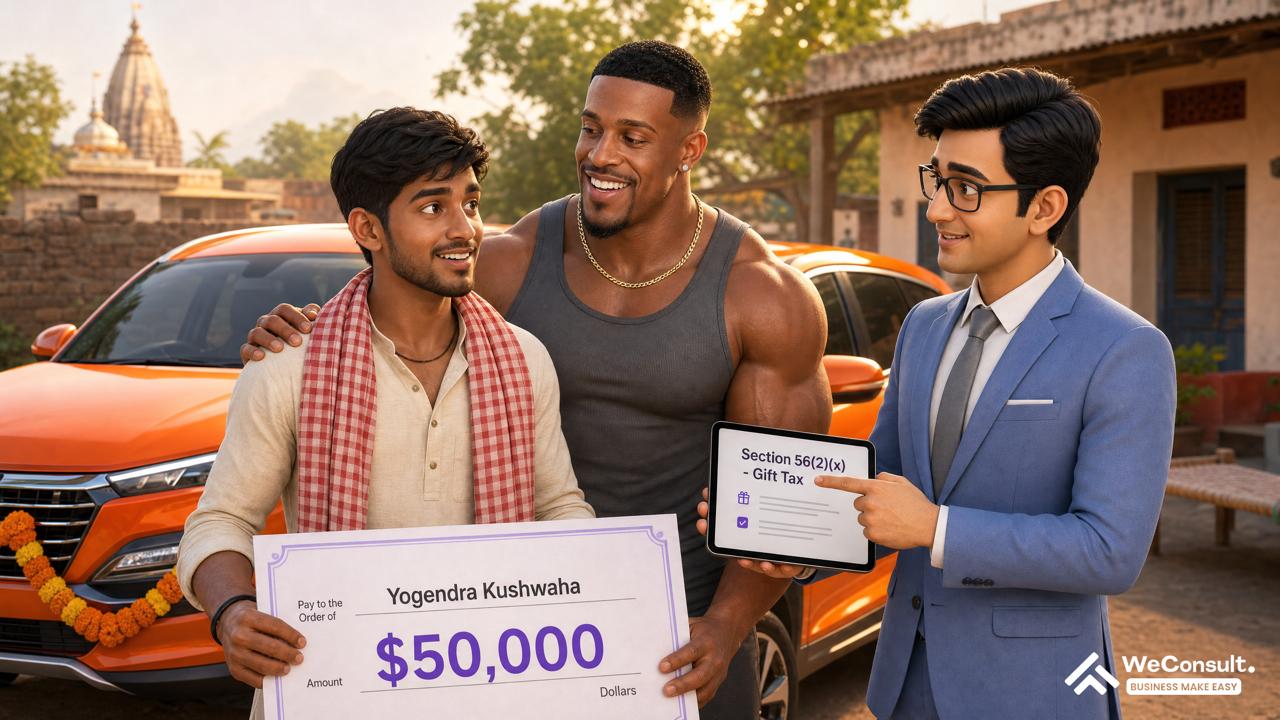

Yogendra Got a Car and $50,000 from Aston Hall — Here Is India's Gift Tax Rule

Published on:

Category: TAX

Author: WeConsult India Desk

The Gift That Changed Everything — and the Tax Nobody Mentioned :

Yogendra did not expect any of this.

A few weeks ago, he was just a young man from a village in India — the kind of person who wakes up early, drinks chai on a kuccha floor, and goes about his day without once imagining a foreign content creator would fly across the world to meet him. Then Aston Hall arrived. The videos went viral. And now, Aston Hall has announced he is gifting Yogendra a car and $50,000 — roughly ₹41.5 lakh at current exchange rates.

The internet cheered. The comments said "blessed." A few people even cried watching the announcement.

Nobody — not one comment, not one news channel — told Yogendra something the Income Tax Act considers important: ₹41.5 lakh received as a gift from a foreign friend is income. And income gets taxed.

The Assumption That Costs People More Than the Original Tax

When a large gift arrives from abroad — especially from someone who is not a blood relative — the joy is immediate. The tax notice, when it comes, usually arrives eighteen months later. By then, the money may already be spent.

Most people in Yogendra's position do the same thing: they receive the funds, celebrate, and assume that because it is a "gift" and not a "salary," the Income Tax Department will not care. That assumption is wrong. And it is an expensive assumption.

Think of it like winning a game show prize. The audience claps. The cameras roll. The host hands you the cheque on live television. But the tax department does not attend the show. They read about it in your ITR the next financial year — and they ask one straightforward question: Did you declare this under Income from Other Sources?

If the answer is no, the follow-up is not a letter. It is a penalty.

What Section 56(2)(x) Actually Says — Without the Jargon

The Income Tax Act, 1961 — and its 2025 successor, the Income Tax Act, 2025 — both carry the same core rule. Under Section 56(2)(x) of the 1961 Act [renumbered as Section 92(2)(m) under the Income Tax Act, 2025], any sum of money received by a resident Indian from a non-relative — whether that person is next door or in a studio in the United States — is taxable as "Income from Other Sources" if the aggregate value in a financial year crosses ₹50,000. [1]

The All-or-Nothing Rule: Once total gifts from non-relatives cross ₹50,000 in a financial year, the ENTIRE amount is taxable — not just the excess.

For Yogendra, the $50,000 cash gift (~₹41.5 lakh) falls squarely in this rule. Aston Hall is a friend, not a relative. The amount far exceeds ₹50,000. The entire ₹41.5 lakh is taxable income in Yogendra's hands.

The car, however, is a different story. Motor vehicles are specifically excluded from the definition of "prescribed movable property" under Section 56(2)(x). [2] The Income Tax Department's own tutorial — as amended by Finance Act 2025 — confirms this: a motor car gifted by a friend attracts no tax under this provision, even if its fair market value exceeds ₹50,000.

The car is tax-free. The cash is not. Welcome to Indian tax law.

|

Regulatory Event |

What It Means for Yogendra — and for You |

|

$50,000 cash gift from foreign friend Aston Hall |

Approx. ₹41.5 lakh added to total income under Sec. 56(2)(x) / Sec. 92(2)(m), ITA 2025 |

|

Aston Hall is a friend, not a "relative" under the Act |

No exemption applies — full ₹41.5 lakh taxable; not just the amount above ₹50,000 |

|

Recipient fails to declare in ITR |

Penalty ₹10,000 to ₹1 lakh; deliberate concealment can attract prosecution [3] |

|

Right move: gift deed + ITR-2 declaration + slab-rate tax paid |

Full compliance, no notice, no interest, no penalty |

Yogendra and Vikram — Two Gifts, Two Different Outcomes:

Yogendra and Vikram both received large sums from foreign friends through social media. Same financial year. Both ordinary Indians — not businessmen, not people who had ever filed a complex ITR before.

Vikram heard about the Yogendra story and was happy for him. He did not connect it to his own situation. He deposited the funds, spent most of it on household repairs and a motorcycle, and filed his usual ITR-1 the following July. His CA asked: "Koi bada transaction tha kya is saal?" Vikram said no. He genuinely did not know the gift counted as income.

Eighteen months later, a notice arrived under Section 148A asking him to explain the large foreign credit in his account.

Yogendra's cousin worked in a CA firm. He called Yogendra the same week the gift was announced and explained the Section 56(2)(x) position. Yogendra came to WeConsult India. The team prepared a gift deed, a bank remittance certificate, and filed ITR-2 correctly, declaring ₹41.5 lakh under Income from Other Sources. Yogendra paid approximately ₹7.8 lakh in tax at his applicable slab rate. He slept fine.

Vikram's notice, by the time interest and penalties were added, cost him more than his original tax liability — plus a two-year assessment proceeding.

The difference between the two outcomes is not which CA they eventually called. It is when they called.

How to Actually Start — 5 Steps for Anyone Who Has Received a Large Gift from Abroad

1. Confirm the donor's relationship with you immediately.

Indian tax law first asks whether the person gifting you money qualifies as a "relative" under Section 56(2)(x). The definition is narrow — parents, siblings, spouse, lineal ascendants and descendants, and their spouses. Friends, however close, are not relatives under the Act. If your donor is a foreign friend or social media contact, assume the gift is taxable and act accordingly.

2. Collect all source documents before the financial year ends.

Gather the foreign inward remittance certificate from your bank, any bank statement showing the credit, a written gift deed (even a simple signed letter confirming the nature of the transfer), and the donor's identity proof if available. Tax authorities scrutinising large foreign credits will ask for all of these. Having them ready prevents a document scramble during assessment.

3. Consult WeConsult India's tax team before you file your ITR.

The correct ITR form for individuals receiving gift income is typically ITR-2, not ITR-1. Filing under the wrong form — or omitting the gift income entirely — are the two most common mistakes in this situation. Getting this right the first time is significantly cheaper than responding to a notice later.

4. Declare the gift correctly under Schedule OS in your ITR.

Under "Income from Other Sources," use Schedule OS in your ITR to declare the gift amount. The amount should match exactly what was credited to your account, converted to INR at the RBI reference rate on the date of receipt. Do not round it down. Do not split it across financial years if it was all received in one year.

5. Mark your ITR filing deadline in your calendar today.

For Financial Year 2025-26, the ITR filing deadline for individuals (non-audit cases) is 31 July 2026. Mark it. Set a reminder for 15 June to start gathering documents. A gift received in May 2026 falls in FY 2025-26 and must appear in the ITR you file by 31 July 2026. That is eleven weeks from today. Enough time — if you start now.

You received something extraordinary. The paperwork to protect it is far simpler than the headline amount suggests.

Key Takeaways

|

Key Compliance Point |

What You Must Do |

|

Cash gift from foreign friend exceeding ₹50,000 is fully taxable |

Declare entire amount under Income from Other Sources in ITR-2 by 31 July 2026 |

|

Car gifted by a foreign friend is not taxable under Sec. 56(2)(x) |

No income tax action needed on the car — keep registration documents clean |

|

Non-declaration attracts penalty of ₹10,000 to ₹1 lakh |

Consult a CA or CS before filing — do not leave it out hoping it goes unnoticed |

|

ITA 2025 renumbers the provision to Section 92(2)(m) |

Same rule, different number — exemptions and threshold remain unchanged |

But Here Is the Other Side…

But here is the other side: Section 56(2)(x) provides a complete exemption for gifts received from specified relatives — regardless of amount. If Aston Hall were Yogendra's brother, father, or brother-in-law, the ₹41.5 lakh cash gift would be entirely tax-free. This matters if you are planning a large family transfer — an NRI parent gifting a child in India, or a sibling abroad sending funds home. In those cases, the relationship must be documented carefully, because the burden of proving the exemption falls on the recipient under Indian law — not the donor.

A Gift Is a Gift — But the Tax Act Was Watching

The Income Tax Act is not designed to punish generosity. It is designed to ensure that money moving into India — however joyfully — is accounted for. Yogendra's situation is one millions of Indians will never face. But the law that governs it applies equally to every resident Indian who receives a foreign transfer from a non-relative above ₹50,000.

If you have received a large amount recently — from a friend, a foreign contact, a social media connection — the first call is not to celebrate. It is to your CA or CS.

WeConsult India's tax advisory team works with first-time ITR filers, NRI families, and individuals navigating unusual income situations across Gurugram's business corridors — from Sector 82 on the Southern Peripheral Road to Udyog Vihar — and for clients across Delhi NCR.

Stay compliant. Stay protected. — WeConsult India

This blog is for informational purposes only and does not constitute legal or professional advice. Please consult a qualified Company Secretary or Chartered Accountant before acting on any compliance matter.

Related Blogs

More articles from the tax.

TAX

Your Family Can Have a Second PAN Card, a Second Tax Return, and a Second Basic Exemption. It Is Called an HUF — and Most Families Have Never Heard of It.

The Story: Suresh is a Gurugram-based businessman. He earns approximately Rs 22 lakh per year — business income plus rental from his father's inherited property. He files one income tax return. He pays tax on Rs 22 lakh. His CA mentioned, almost in passing: You should consider forming an HUF. What his CA did not say clearly enough is that Suresh's family qualifies to form an HUF right now, today — and that by doing so, he could legally transfer the rental income to a separate tax entity, file a second income tax return, claim a second basic exemption limit, and reduce his family's total tax burden by approximately Rs 1.5 lakh every year. Every year. Indefinitely. Not a scheme. Not a loophole. A legal tax entity specifically created by the Income Tax Act and recognised for over a century of Indian tax law. The Real Problem — Why Most Families Never Form an HUF Most people associate HUFs with large joint families in ancestral havelis managing farmland. The modern reality is entirely different. Any Hindu married man — and his wife and children — automatically constitutes a Hindu Undivided Family the moment he marries. The HUF exists as a legal concept from the moment of marriage. What most people never do is recognise that HUF by obtaining a separate PAN card and filing a separate income tax return for it. Think of it this way: the Income Tax Act treats an HUF as a completely separate taxpayer — like a separate company or a separate individual. It gets its own PAN. It files its own ITR. It gets its own basic exemption limit. It gets its own slab rates. For a family in the 20-30% tax bracket, transferring eligible income to the HUF can move that income into the 5-10% bracket — or entirely within the exemption limit. The confusion is not about eligibility. Almost every Hindu married family in India is eligible. The confusion is about which income can legitimately go into the HUF — and which cannot. The Law Explained Simply — What an HUF Is and How It Is Taxed An HUF is a distinct legal and tax entity recognised under Hindu law and specifically under the Income Tax Act, 2025. It consists of all persons lineally descended from a common ancestor — and their wives and unmarried daughters. Who can form an HUF: Any Hindu male who is married (he becomes the Karta — the manager). His wife, children, and their dependants are members. Sikhs, Jains, and Buddhists can also form HUFs. Muslims, Christians, and Parsis cannot. Even a couple without children can form and operate an HUF. What CAN go into the HUF: (1) Ancestral property — received by inheritance from father, grandfather, or great-grandfather. (2) Gifts from non-members — relatives up to Rs 50,000 per occasion tax-free; non-relatives taxable if aggregate exceeds Rs 50,000 in a year. (3) HUF business income. (4) Income from assets held in the HUF's name. What CANNOT go into the HUF: (1) Salary income — cannot be transferred, will be clubbed back under Section 64. (2) Professional income — doctor's fees, consultant invoices — individual skills-based, cannot be assigned. (3) Self-acquired property income transferred by the Karta — income clubbed back. Only ancestral property or genuinely gifted assets belong in the HUF. Income Slab Tax Rate (New Regime) Notes Up to Rs 3 lakh Nil HUF basic exemption — separate from individual Rs 3 lakh – Rs 7 lakh 5% Same as individual new regime Rs 7 lakh – Rs 10 lakh 10% Lower than individual's marginal rate if HUF income is separated Rs 10 lakh – Rs 12 lakh 15% HUF files ITR-2 or ITR-3 separately Above Rs 15 lakh 30% Identical to individual slab structure Suresh's Family — Before and After HUF Without HUF: Suresh's total income Rs 22 lakh (business Rs 18 lakh + rental Rs 4 lakh). One ITR. Tax under new regime: approximately Rs 3.3 lakh. With HUF (ancestral property rental in HUF's name): Suresh's individual income: Rs 18 lakh. Tax: approximately Rs 2.6 lakh. HUF income: Rs 2.16 lakh net rental (after 30% standard deduction). Tax: Nil — within Rs 3 lakh basic exemption under new regime. Total family tax: Rs 2.6 lakh versus Rs 3.3 lakh without HUF. Annual saving: approximately Rs 70,000 — just from recognising the HUF on one ancestral property. For a family where the HUF has Rs 8-10 lakh of eligible income, the annual saving can be Rs 1.5-2.5 lakh. How to Actually Start — 5 Steps to Form and Operate Your HUF 1. Step 1 — Execute an HUF Deed — An HUF is formed by a formal declaration — a written deed executed on stamp paper, signed by the Karta. The deed declares the existence of the HUF, names the Karta, names all members (coparceners), and identifies the initial corpus (typically the ancestral property or initial gifted corpus). The deed is a private document — not registered with any government authority — but it is the foundational document for every subsequent step. WeConsult India drafts HUF deeds as part of the formation package. 2. Step 2 — Apply for a PAN for the HUF — The HUF is a separate taxpayer and needs its own Permanent Account Number. Apply using Form 49A at any NSDL/UTI PAN application centre — online or offline. The application requires the HUF deed, the Karta's existing PAN, Aadhaar, and address proof. PAN is typically issued within 5-7 working days. Once the HUF has a PAN, it can open a bank account, make investments, and conduct financial transactions in its own name. 3. Step 3 — Open a bank account in the HUF's name — Every HUF needs a separate current or savings account opened in the name of Suresh HUF (the convention is [Karta's name] HUF). The Karta operates the account as manager of the HUF. This account is where the HUF's income is received — rental income, interest, dividends, gifted funds — and from where HUF expenses and investments are made. 4. Step 4 — Transfer eligible income-generating assets to the HUF — Only ancestral property or gifted assets can be legitimately transferred to the HUF. Self-acquired property cannot be transferred without triggering clubbing under Section 64. Consult WeConsult India or your CA before transferring any asset to confirm it qualifies. The asset transfer is documented by a formal transfer deed or gift deed. Once transferred, all income from that asset belongs to the HUF and is taxed in the HUF's hands. 5. Step 5 — File a separate ITR for the HUF every year — The HUF files its own income tax return — ITR-2 (investment and rental income only) or ITR-3 (if business income). Same filing deadlines as individuals: July 31 for non-audit cases, October 31 for audit cases. The HUF also has its own advance tax obligations if tax liability exceeds Rs 10,000 in a financial year. Maintain the HUF's accounts separately — every income and expense must be documented and traceable to the HUF's bank account and PAN. Your family is already an HUF. The question is only whether you have recognised it and put it to work. Key Takeaways Key Compliance Point What You Must Do An HUF is a separate tax entity with its own PAN and its own basic exemption limit Execute an HUF deed, apply for HUF PAN, and open a separate HUF bank account — in that order Only ancestral property and gifted assets can be placed in the HUF — not salary or professional income Confirm which income sources qualify before transferring any asset — clubbing provisions under Section 64 are strictly enforced The HUF must file its own ITR every year — separate from individual members File the HUF's ITR by July 31 each year. The HUF also has its own advance tax obligations if liability exceeds Rs 10,000 HUF formation is legal, recognised, and available to almost every Hindu married family in India Form the HUF this financial year — every year without one is a year of excess tax paid that cannot be recovered But Here Is the Other Side… But here is the other side: the HUF structure has real limitations and a few active traps. First, the clubbing provisions under Section 64 are aggressively enforced — any income from self-acquired assets transferred to the HUF, or any salary income routed through the HUF, will be clubbed back to the individual's income. Second, a partition of the HUF — when members decide to split the HUF's assets — can be a complex and tax-triggering event with capital gains consequences. Third, under the new tax regime (the default), the HUF cannot claim most deductions under Chapter VI-A — including 80C, 80D, and HRA. The tax benefit works best when the HUF's income is in the lower slabs, not when it is large enough to push into higher brackets. Fourth, the HUF is a long-term structure that becomes more complex to manage over generations as membership expands. The HUF is a legitimate and powerful tool — but it works best when structured correctly from the start, not when retrofitted around existing income flows after the fact. One Last Thing — The HUF Already Exists. You Just Haven't Registered It. Suresh's HUF came into existence the day he married. Under Hindu law, the moment a Hindu male marries, an HUF is constituted — consisting of himself, his wife, and any future children. The HUF has been there for years. It has simply been unrecognised. Every year that passes without recognising and operating the HUF is a year in which Suresh's family has paid more tax than the law requires them to pay. The new regime's Rs 3 lakh basic exemption is available to the HUF separately — not shared with Suresh's individual return. Two exemptions. Two sets of slab rates. One family. The HUF deed takes one week to draft and execute. The PAN application takes five working days. The bank account takes one week. The total cost of HUF formation: Rs 10,000-20,000 in professional fees. The annual tax saving: Rs 70,000 to Rs 2.5 lakh, every year, for the life of the HUF. WeConsult India forms HUFs, drafts HUF deeds, files HUF PAN applications, and manages annual HUF income tax returns for families across Gurugram's Sector 82, Sector 84, and the Udyog Vihar corridor. Stay compliant. Stay protected. — WeConsult India This blog is for informational purposes only and does not constitute legal or professional advice. Please consult a qualified Company Secretary or Chartered Accountant before acting on any compliance matter.

TAX

GSTR-1 Is Due Today — And One Old Return Is Closing Forever

🔴 TWO DEADLINES TODAY DEADLINE ALERT: GSTR-1 for April 2026 is due today, May 11. And April 2023 GSTR-1 locks permanently after today under Section 37, CGST Act. Two deadlines. Same date. Most businesses know only one. The Two Deadlines Nobody Told You About Vikram opened the GST portal this morning expecting a routine task. GSTR-1 for April 2026 — he has done this eleven times now. His accountant had already sent a WhatsApp: Sir, GSTR-1 today. He clicked through to the Returns Dashboard and started preparing the April entries. Forty minutes, maybe less. What Vikram did not notice was a second line on the same dashboard, sitting quietly in the historical returns section. April 2023. Status: Not Filed. [EXPERIENCE SIGNAL] The kind of compliance gap that costs a business its entire ITC trail for a month does not happen because anyone was dishonest. It happens because April 2023 was a month of team transitions — and nobody had the presence of mind to look backward when they were busy looking forward. That return has been sitting there for three years. Today is the last day anyone can touch it. After today, the GST portal will block it — permanently, with no override, no appeal, and no late-fee payment that can reopen it. What Most Businesses Are Missing Right Now Most business owners know GSTR-1 is due on the 11th of every month. File outward supplies, generate GSTR-2B for buyers, move on. That is deadline number one — April 2026 GSTR-1, due today. Deadline number two is quieter. Under Section 37 of the CGST Act, 2017, as amended by the Finance Act 2022, no GSTR-1 can be filed more than three years after its original due date. For April 2023, that due date was May 11, 2023. Three years from that date is exactly today. After today, the portal will not accept the April 2023 return — not for any reason, and not for any amount. The wrong reaction is to treat today as a single-task day. The 3-year lock has been running silently since 2022. Month by month, old returns have been closing. March 2023 closed on April 11, 2026. April 2023 closes today. May 2023 will close on June 11, 2026. Think of your unfiled old returns as a time-locked vault inside a bank. You know you need to make a deposit today — that is the April 2026 filing. But there is a second compartment from 2023, set to seal shut at a fixed time. Once the timer runs out, not even the bank manager can open it. The bank does not destroy the records. It just makes them permanently inaccessible. What the Law Actually Says Under Section 37 of the CGST Act, 2017 — as amended by the Finance Act 2022 — a registered taxpayer cannot file a GSTR-1 return after three years from its original due date. This is not a penalty provision. It is a hard portal block. Once the window closes, the system will not accept the return regardless of the reason for non-filing. A GSTR-1 return is like a shipping manifest sent to a freight exchange. Until your manifest arrives, your buyers cannot confirm their cargo. Once you file, their GSTR-2B is updated on the 14th — and they can claim Input Tax Credit. If you do not file, they cannot claim. And if the portal locks your old return, no invoice or payment record will restore the ITC chain. Regulatory Event What It Means for Your Business Section 37 CGST Act — 3-year portal lock (Finance Act 2022) April 2023 GSTR-1 (due May 11, 2023) cannot be filed after today — portal permanently blocks access GSTR-1 for April 2026 due today Monthly filers with turnover above ₹5 crore must file today; late fee ₹50/day from tomorrow under Section 47 CGST Act [1] Late GSTR-1 blocks buyer ITC Your buyers cannot claim April 2026 ITC in GSTR-2B (generated May 14) until you file your GSTR-1 today GSTR-3B now hard-locked from GSTR-1 From July 2025, Table 3 in GSTR-3B is auto-populated from GSTR-1 and cannot be manually overridden — accuracy today is non-negotiable [2] What Happened to Vikram — and What Priya Did Differently Both Vikram and Priya own mid-sized manufacturing firms in Gurugram, both with turnovers above ₹5 crore. Both had a difficult April 2023 — a finance team changeover, vendor disputes, and a busy quarter-close. In both companies, the April 2023 GSTR-1 slipped. Nobody noticed at the time. This morning, Priya's team pulled a historical return status report before starting today's filing. The April 2023 gap came up. They filed it immediately — paid the applicable late fee of ₹50 per day for the period of default [1]. That is not a small amount. But it is manageable. And her buyers' ITC trail for that month stayed intact. Vikram filed April 2026 GSTR-1, closed the laptop, and moved on. By evening, the April 2023 window will have closed. The ₹14 lakh worth of B2B invoices from that month — supplies made to four customers — will never appear in any GSTR-2B. If any of those customers raise an ITC dispute today, Vikram has no portal-level path to correct it. The difference is not which CA they had. It is whether anyone thought to look backward today before looking forward. How to Start Right Now — Five Steps 1. Check April 2026 GSTR-1 status immediately — Log in to gst.gov.in, go to Returns > Returns Dashboard, select April 2026, and confirm GSTR-1 status. If not filed, begin immediately. Monthly filers have until today. Every hour matters — the portal slows under peak traffic near deadlines. 2. Pull a historical return status check before closing the tab — On the same portal, go to Returns > View Filed Returns. Check every month from April 2023 onward. Any Not Filed status from April 2023 is in the final window today. May 2023, June 2023, and beyond have their own closing dates — but April closes tonight. 3. Contact WeConsult India if any historical return shows unfiled — Do not attempt to backfile without first reviewing the ITC implications, applicable late fees, and correct filing sequence. WeConsult India can assess your position and guide you through the process before the window closes. A 30-minute call today could prevent a three-year liability becoming permanent. 4. Brief your accountant on the GSTR-3B hard-lock — From the July 2025 tax period onward, GSTR-3B Table 3 is auto-populated from your GSTR-1 data and cannot be manually overridden [2]. Any error in today's GSTR-1 must be corrected through GSTR-1A before you file GSTR-3B on May 20. Make sure your team knows this workflow before May 20 arrives. 5. Set a reminder for May 20 today — GSTR-3B for April 2026 is due on May 20, 2026. Mark it now. The data you submit in GSTR-1 today directly determines what auto-populates in GSTR-3B in nine days. If both returns are filed correctly, your buyers see clean ITC — and your FY 2026-27 compliance starts on solid ground. Key Takeaways Key Compliance Point What You Must Do GSTR-1 for April 2026 is due today, May 11 File before the day ends — late fee is ₹50/day from tomorrow under Section 47, CGST Act April 2023 GSTR-1 permanently locks after today Check historical return status now — this is the absolute last filing window for that period GSTR-3B Table 3 is auto-populated and hard-locked from GSTR-1 Correct errors in GSTR-1A before filing GSTR-3B on May 20, 2026 Late GSTR-1 blocks buyer ITC chain Your B2B buyers cannot claim April ITC in GSTR-2B until your GSTR-1 is filed today But Here Is the Other Side... the 3-year lock under Section 37 of the CGST Act prevents filing the return on the portal — it does not automatically extinguish a taxpayer's right to claim that a supply was made. In cases where a business has original invoices, e-way bills, and payment evidence showing genuine transactions for April 2023, the GST Appellate Tribunal has in some cases considered ITC disputes on merit, separate from the portal filing record. This matters if your buyers have already raised a formal ITC dispute on April 2023 supplies — a professional review is necessary before concluding that all remedies are permanently closed. You Are Already Doing More Than You Know Compliance in India is not designed to trap honest businesses. It is designed to create a paper trail that matches actual commerce. If you are filing GSTR-1 every month and keeping invoices, you are doing the fundamentals right. Today is about making sure one old gap does not become permanent before anyone noticed it was open. WeConsult India works with businesses across Gurugram's newer commercial clusters — including companies in Sector 82, Sector 84, and the Southern Peripheral Road corridor — where growing teams and frequent accountant transitions often leave historical GST filing gaps undetected until deadlines like today surface them. If your company has any unfiled GSTR-1 returns from FY 2022-23 or FY 2023-24, today may be your last window for the earliest months. Stay compliant. Stay protected. — WeConsult India This blog is for informational purposes only and does not constitute legal or professional advice. Please consult a qualified Company Secretary or Chartered Accountant before acting on any compliance matter.

TAX

Most Business Owners Think May Has One Compliance Deadline. It Has Eight. Here Is Every Date Before May 31.

The Story: Rajan runs a small manufacturing unit in Gurugram's IMT Manesar. Twelve employees on payroll, GST-registered, TDS deductor, EPFO and ESIC registered. In his mind, May's compliance is simple: GSTR-3B by the 20th. That is the one date he has written on his whiteboard every May. May 2026 has seven more compliance deadlines he has not written anywhere. And the biggest one is May 31 — the quarterly TDS return filing that is unlike anything he has filed before. For most employers and deductors, the largest deadline of the month is May 31, when the Q4 TDS returns for January-March 2026 are due in Forms 24Q, 26Q, and 27Q. If he misses it: Rs 200 per day per return. For three returns, that is Rs 600 per day, accumulating with no ceiling, until the returns are filed. This blog is Rajan's whiteboard for May 2026. The Real Problem — Why Business Owners Chronically Underestimate May May feels quiet. The financial year just closed. The annual return season is months away. Advance tax doesn't start until June 15. Income tax return season is July. But May is the month that closes Q4. Quarterly TDS returns for January-March across every form. PF and ESI for April payroll. First month of GST returns for the new financial year. Several other filings landing quietly between the 10th and the 31st. Think of May as the month where both doors are open simultaneously: the exit door of the old financial year and the entrance door of the new one. Filings come through both doors at once. If you are only watching the entrance — GSTR-3B on the 20th — everything coming through the exit door piles up unnoticed until the last week. The Complete May 2026 Compliance Map — 8 Deadlines, Date by Date Date Filing Who Files Late Penalty May 7 (passed) TDS/TCS deposit — April 2026 All TDS deductors 1.5% per month interest May 11 GSTR-1 — April 2026 Monthly GST filers (AATO > Rs 5 crore) Rs 50/day May 13 GSTR-7 / GSTR-8 GST TDS deductors / e-commerce TCS collectors Rs 50/day May 15 PF + ESI — April 2026 payroll All EPFO + ESIC registered employers 12-25% per annum interest May 15 Form 27EQ — Q4 TCS return TCS collectors Rs 200/day May 20 GSTR-3B — April 2026 Monthly GST filers Rs 50/day + 18% interest on tax May 25 PMT-06 — April 2026 QRMP scheme taxpayers only 18% interest May 30 LLP Form 11 — FY 2025-26 All LLPs (even with nil transactions) Rs 100/day — no ceiling MAY 31 Q4 TDS Returns 24Q (salary) + 26Q (non-salary) + 27Q (non-resident) All TDS deductors — employers + businesses with vendors Rs 200/day PER FORM — no ceiling. 3 forms = Rs 600/day. Each Deadline Explained May 11 — GSTR-1 for Monthly Filers Every invoice, credit note, and debit note you issued to customers in April must be uploaded here. This is the form your buyers depend on for their GSTR-2B auto-population. If you are late with GSTR-1, your buyers' ITC in GSTR-2B will be short — and under the new ITC Hard Block, their GSTR-3B filing may be blocked. If your AATO is above Rs 5 crore and you have not configured e-invoicing, every invoice you upload should already carry an IRN. May 15 — PF + ESI Contributions PF and ESI deposits for April 2026 salary are due May 15. Both the employee share (deducted from salary) and employer share (contributed by the company) must be deposited. Delayed PF deposits attract interest of 12-25% per annum. Aadhaar and PAN validation is mandatory on the ECR — if any employee's details are not validated in the EPFO system, their contribution will not credit correctly. May 20 — GSTR-3B (The One Rajan Knows) GSTR-3B is the summary GST return covering outward supplies, ITC claims, and net tax payment for April 2026. Under the ITC Hard Block active from April 1, 2026 — if your ITC claim exceeds your GSTR-2B auto-populated figure, the portal blocks filing entirely. Reconcile GSTR-2B against your purchase register before attempting to file. Defer any unmatched ITC rather than risk a blocked return. May 30 — LLP Form 11 Limited Liability Partnerships must file Form 11 (LLP Annual Return) for FY 2025-26 by May 30, 2026. Form 11 contains details of all designated partners, contributions, and any change in partner composition during the year. Penalty for missing it: Rs 100 per day of default with no upper cap. Even an LLP with no transactions in FY 2025-26 must file. May 31 — Q4 TDS Returns (The One Most Business Owners Miss) The largest deadline of the month. Forms 24Q, 26Q, and 27Q for the quarter January-March 2026. Form 24Q (Salary TDS): Q4 is the most data-intensive quarter — includes Annexure-II with annual employee-wise reconciliation of salary, deductions, tax regime, and total TDS. This Annexure-II data generates Form 16 Part B via TRACES. Late Q4 filing directly delays Form 16 issuance to employees — disrupting their ITR filing, home loan applications, and visa documentation. Form 26Q (Non-salary TDS): All TDS deducted on vendor payments — contractor payments, professional fees, rent, interest — between January and March 2026. Form 27Q (TDS on non-resident payments): If your business made any payments to foreign vendors, consultants, or suppliers between January and March 2026. Critical 2026 transition note: Q4 returns use ITA 1961 — while April 2026 deductions use ITA 2025. Forms 24Q, 26Q, and 27Q for Q4 must reference ITA 1961 section numbers (192, 194C, 194J, 194I). Do not use ITA 2025 references (392, 393) in a May 31 Q4 return. The governing Act is determined by when the income was earned — not when the return is filed. Key Takeaways Key Compliance Point What You Must Do May 31 is the largest deadline — Q4 TDS returns (24Q, 26Q, 27Q) Start Q4 data reconciliation today. Salary data, vendor payments, PAN verification — all must be clean before filing Q4 TDS returns are filed under ITA 1961 — not ITA 2025 Use old section numbers: 192 (salary), 194C (contracts), 194J (professional fees). Do NOT use Section 392/393 in a May 31 Q4 return Form 16 issuance depends on May 31 Q4 filing Late Q4 filing pushes Form 16 issuance past June 15 — directly disrupting employees' ITR filing, home loan, and visa documentation LLP Form 11 due May 30 — often missed If your business is an LLP — even one with no transactions in FY 2025-26 — Form 11 is mandatory. Rs 100/day late fee, no ceiling But Here Is the Other Side… But here is the other side: for very small businesses — sole proprietorships, small traders on the GST composition scheme, businesses without employees — May's compliance load is genuinely lighter. A composition scheme taxpayer's CMP-08 for Q4 was due April 18 — nothing major in May. A business without employees has no PF, ESI, or Form 24Q obligations. A business with no non-resident vendors skips Form 27Q. The eight deadlines above do not all apply to every business simultaneously. But every GST-registered, TDS-deducting employer in India with at least one vendor relationship is managing six or more of these simultaneously — and the only safe assumption is that each one applies until you have specifically confirmed it does not. One Last Thing — May 31 Is Three Weeks Away. Start the Q4 Data Pull Today. The Q4 TDS return process — especially Form 24Q with Annexure-II — is the most data-intensive filing in the annual compliance calendar. It requires employee-wise salary reconciliation, regime-wise deduction mapping, PAN verification for every deductee, and month-by-month TDS reconciliation against challans deposited between January and March. Starting this on May 29 is not starting it. Starting it today is what makes May 31 manageable. WeConsult India handles Q4 TDS return filing — Forms 24Q, 26Q, and 27Q — for companies across Gurugram's IMT Manesar, Sector 37, and Udyog Vihar. We also manage Form 16 generation and TRACES download for all employees after Q4 filing. If you have not yet started your Q4 data reconciliation, contact us today. Stay compliant. Stay protected. — WeConsult India This blog is for informational purposes only and does not constitute legal or professional advice. Please consult a qualified Company Secretary or Chartered Accountant before acting on any compliance matter.